Breathe Easier With These Home Mortgage Tips

Written by-Jimenez BowlesIf you're looking into home mortgages, then you surely are excited. It's time to buy a home! However, what you might realize is there is quite a lot of information to take in, and how do you sort all of this out to get to the mortgage company and product that you need? Keep reading to find out how to do this.

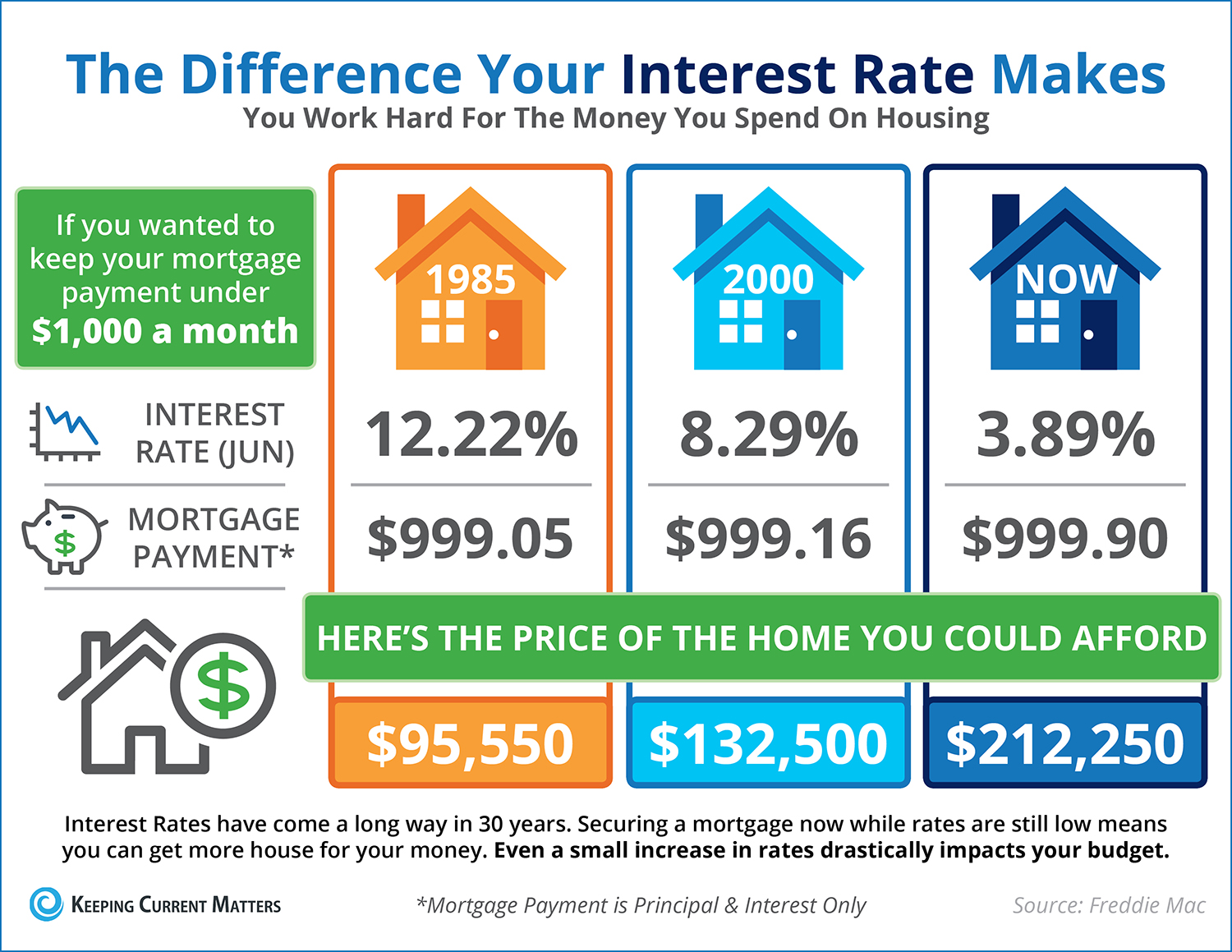

When it comes to getting a good interest rate, shop around. Each individual lender sets their interest rate based on the current market rate; however, interest rates can vary from company to company. By shopping around, you can ensure that you will be receiving the lowest interest rate currently available.

Save enough money to make a down payment. Lenders may accept as little as 3.5% down but try to make a larger down payment. If you put down 20% of your total mortgage, you won't have to pay private mortgage insurance and your payments will be lower. You will also need cash to pay closing costs, application fees and other expenses.

If a 20% down payment is out of your league, do some shopping around. Different banks will have different offers for you to consider. Terms and rates will vary at each, some will give a lower downpayment, but a slightly higher interest rate. Look for the best mix for your current situation.

If your financial situation changes, you may not be approved for a mortgage. Don't apply to get a mortgage unless you have a steady job. You ought not get a new job until you're approved for your mortgage, since the lender will make a decision based to the information on your application.

Make sure you know how much you can afford before applying for a mortgage. Do not rely on what your lender says you can afford. Make a budget, allowing room for any unexpected expenses. Use online calculators which can help you estimate how much mortgage you can afford to pay monthly.

In order to be eligible to a home mortgage, you need to show a stable work history over the long term. A steady work history is important to mortgage lenders. If you frequently change jobs, a lender will most likely not approve the loan. Do not quit your job while you are involved in the mortgage loan process.

Try giving your lender a chance to help you with mortgage payment problems. If you struggle to make payments, do not ignore your lender's services. There are various new programs to help you keep up with your mortgage payments like forbearance if you have an FHA mortgage. Lenders are generally happy to work out any delinquent loans via loan modifications, or possibly short sales if you can't afford to keep your home. It can be difficult to deal with them over this, but communication is key.

Know your mortgage interest rate type. When you are obtaining home financing you should understand how the interest is calculated. Your rate could be fixed or it could be adjustable. With fixed interest rates, your payment will usually not change. Adjustable rates vary depending on the flow of the market and are variable.

If you are a first time home owner, get the shortest term fixed mortgage possible. The rates are typically lower for 10 and 15 year mortgages, and you will build equity in your home sooner. If you need to sell you home and purchase a larger one, you will have more cash to work with.

Don't use real estate brokers or mortgage lenders who encourage you to lie on your home mortgage application. It is illegal to lie on this application, and it is a legal document. Misrepresenting your income or other information is grounds for criminal prosecution. Working with people who encourage you do commit a crime is not a good idea.

https://business.chase.com/resources/manage/equipment-financing on home mortgages are lower than they have been in years. click the up coming web site expect them to begin increasing again shortly, so now is a great time to purchase a home and finance it at a low rate. The shorter the term of the mortgage, the better the rate you will be able to get.

If you are a retired person in the process of getting a mortgage, get a 30 year fixed loan if possible. Even though your home may never be paid off in your lifetime, your payments will be lower. Since you will be living on a fixed income, it is important that your payments stay as low as possible and do not change.

Do not even consider getting a home mortgage that is only paying the interest. This is the worst possible investment that you can make. The problem is that you are not getting any closer to actually owning your home. Instead, purchase a home that you can afford to pay principle on so that you are truly making a good investment.

If your downpayment is less than 20% of the sales price of the home you want to buy, expect the mortgage lender to require mortgage insurance. This insurance protects the lender in the event that you can't pay your mortgage payments. Avoid mortgage insurance premiums by making a downpayment of at least 20%.

Investigate preapprovals before you start home shopping. Preapproved mortgages will give you an idea of both how much home you can afford plus what your monthly mortgage payments will be. This will set the parameters of your home shopping and save you time not looking at properties you can't realistically afford.

Keep on top of your mortgage application by checking in with your loan manager at least once per week. It only takes one missing piece of paperwork to delay your approval and closing. There may also be last minute requests for more information that need to be provided. Don't assume everything is fine if you don't hear from your lender.

There are times when the seller of a home will be able to give you a land contract so you can purchase the home. The seller needs to own the home outright, or owe very little on it for this to work. A land contract may need to be paid within a few years.

Now that you know so much about home mortgages, you should have no problem attaining one in the future. This will ensure that you can afford the home you need, plus it will help you save money. Once you've moved in, you'll be so pleased that you took the time to read this article.